Estate Planning

by Admin

Posted on 14-03-2025 10:33 AM

:max_bytes(150000):strip_icc()/Dispute-resolution-resized-7293f1fe491a458d895586fd27292686.jpg)

Importance of Estate Planning

Estate planning is crucial for individuals of all ages and income levels. It helps to ensure that their assets are distributed according to their wishes, rather than being decided by a court. Without an estate plan, an individual's assets may be subject to probate, which can be a lengthy and expensive process. Estate planning also helps to minimize taxes and legal fees, which can save an individual's loved ones a significant amount of money. Additionally, estate planning can help to avoid family conflicts and ensure that an individual's wishes are respected.

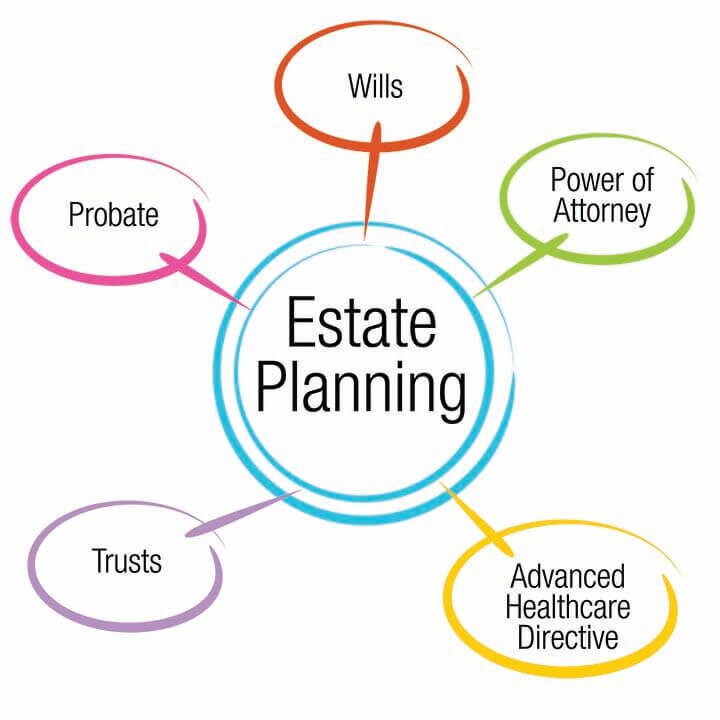

Components of an Estate Plan

An estate plan typically includes several components, such as a will, trusts, powers of attorney, and beneficiary designations. A will is a document that outlines how an individual's assets should be distributed after their death. Trusts are legal arrangements that allow an individual to manage and distribute their assets according to their wishes. Powers of attorney give an individual the authority to make decisions on behalf of another person, such as managing their finances or making medical decisions. Beneficiary designations are used to designate who will receive an individual's assets, such as life insurance policies or retirement accounts.

Types of Trusts

There are several types of trusts that can be used in estate planning, including revocable trusts, irrevocable trusts, and charitable trusts. Revocable trusts are trusts that can be changed or terminated during an individual's lifetime. Irrevocable trusts are trusts that cannot be changed or terminated once they are created. Charitable trusts are trusts that are used to make donations to charity. Each type of trust has its own advantages and disadvantages, and an individual should consult with an attorney to determine which type of trust is best for their situation.

Types of Powers of Attorney

There are several types of powers of attorney that can be used in estate planning, including durable powers of attorney, springing powers of attorney, and limited powers of attorney. Durable powers of attorney are powers of attorney that remain in effect even if an individual becomes incapacitated. Springing powers of attorney are powers of attorney that only become effective if an individual becomes incapacitated. Limited powers of attorney are powers of attorney that give an individual the authority to make decisions on behalf of another person for a specific purpose or period of time.

Estate Planning for Specific Situations

Estate planning can be more complex for individuals in certain situations, such as those with minor children, those who are married, or those who own a business. For individuals with minor children, estate planning may involve creating a trust to manage their assets until they reach adulthood. For those who are married, estate planning may involve creating a joint trust or making beneficiary designations to ensure that their spouse inherits their assets. For business owners, estate planning may involve creating a business succession plan to ensure that their business is transferred to the next generation or sold to a third party.

Estate Planning for Minor Children

Estate planning for minor children involves creating a plan that outlines how their assets will be managed and distributed until they reach adulthood. This may involve creating a trust to manage their assets, such as a minor's trust or a custodial account. It may also involve naming a guardian to care for them if their parents are unable to do so. Estate planning for minor children can help to ensure that they are taken care of and that their assets are protected until they are old enough to manage them themselves.

Estate Planning for Business Owners

Estate planning for business owners involves creating a plan that outlines how their business will be transferred to the next generation or sold to a third party. This may involve creating a business succession plan, which outlines how the business will be transferred and who will be responsible for managing it. It may also involve creating a buy-sell agreement, which outlines how the business will be sold if one of the owners dies or becomes incapacitated. Estate planning for business owners can help to ensure that their business is transferred smoothly and that their loved ones are taken care of.

Tax Planning

Tax planning is an essential part of estate planning. It involves creating a plan that minimizes taxes and ensures that an individual's assets are distributed according to their wishes. This may involve creating a trust to minimize estate taxes, or making charitable donations to reduce income taxes. Tax planning can help to save an individual's loved ones a significant amount of money and ensure that their assets are protected from unnecessary taxes.

Probate and Estate Administration

Probate and estate administration involve the process of managing and distributing an individual's assets after their death. This may involve creating an inventory of their assets, paying their debts, and distributing their assets according to their will or trust. Probate and estate administration can be a lengthy and expensive process, but it can be avoided with proper estate planning.

It seems like you forgot to provide the anchor text and URL. Please provide them, and I'll be happy to help you add the anchor to the paragraph.

FAQs

What is estate planning?

Estate planning is the process of managing and distributing an individual's assets after their death or incapacitation. It involves creating a plan that outlines how to manage and distribute their assets according to their wishes.

Why is estate planning important?

Estate planning is important because it helps to ensure that an individual's assets are distributed according to their wishes, rather than being decided by a court. It also helps to minimize taxes and legal fees, which can save an individual's loved ones a significant amount of money.

What are the components of an estate plan?

The components of an estate plan typically include a will, trusts, powers of attorney, and beneficiary designations. A will is a document that outlines how an individual's assets should be distributed after their death. Trusts are legal arrangements that allow an individual to manage and distribute their assets according to their wishes.

What is the difference between a will and a trust?

A will is a document that outlines how an individual's assets should be distributed after their death, while a trust is a legal arrangement that allows an individual to manage and distribute their assets according to their wishes. A trust can be used to avoid probate and minimize taxes, while a will is subject to probate and may be subject to taxes.

How often should I review my estate plan?

It is recommended that individuals review their estate plan every 5-10 years, or whenever there is a significant change in their life, such as a marriage, divorce, or the birth of a child. This can help to ensure that their estate plan is up-to-date and reflects their current wishes and circumstances.

Odom Law Group

24801 Pico Canyon Road

Suite 100 & 300

Santa Clarita, CA 91381

(661) 367-1699